The next $100B data company will be embedded.

You’ve used embedded analytics today and can’t name who built it.

That’s not an accident. It’s the sales pitch.

WisdomAI sells itself with five words: “Your users never see WisdomAI.” DataBrain promises the same: “Your users never know it’s DataBrain powering their analytics.”

Embedded analytics lives inside somebody else’s app, wears somebody else’s logo, and succeeds by disappearing. No wonder even the people paid to measure the market can’t agree what they’re looking at. One research camp puts the market at $23 billion in 2025. Another at $78 billion.

And I think both numbers are too small. Not by percent, by multiples.

I’ve always been excited about embedded analytics for one reason: it sells much closer to actual value than most of the data industry does.

Most data companies sell another tool to a data team. Then the data team has to get somebody else to use it, change a decision, change a workflow, and somehow create value at the end of that chain.

Embedded skips half of that mess.

Inside a large enterprise, it makes the software people already work in smarter. The data team becomes an enabling layer behind the product instead of the final customer desperately trying to drive adoption.

Inside a product company, it makes the actual product customers pay for smarter.

One path improves the tools a company runs on. The other improves the thing it sells. Either way, the route from analytics to value is unusually short.

And now, agentic happened.

The same short route to value. Suddenly multiplied.

That is why I think this is the biggest open opportunity in data.

BUT “open” is doing a lot of work there.

The same thing that makes embedded analytics enormous, living invisibly inside other people’s products, also creates three hard problems. Nobody asks for the invisible vendor by name. Every customer wants its learning sealed off from everyone else’s. And BI incumbents still treat embedded like a stepchild.

Solve those, and I think you have a shot at the next $100B data company.

I think you should: go build there, get a job there, or move your existing analytics company there before everybody else notices.

Agentic multiplies the market twice

A dashboard waits for someone to open it. An embedded agent lives inside a product people already use, and is proactive rather than reactive.

That’s the first multiplier: reach. Embedded analytical agents reach the salesperson inside the CRM, the operator inside the logistics product, the customer inside the support tool, without anyone opening up a dashboard they didn’t care about. Roughly 10x more people than dashboards ever touched.

The second multiplier: value. A chart shows you something. An agent does the analysis, picks the next step, takes the action, watches what happened, and gets better. Roughly 10x more value per user.

10 × 10 = 100.

Argue with the tens if you want. Make them threes and you still get a 9x market.

Everybody can see Snowflake. Everybody can see Databricks. Nobody is pricing the market multiplying underneath them.

So why hasn’t everybody already won it?

What keeps it open: three unsolved problems

Problem 1: Nobody asks for an invisible company. This is the Intel Inside problem. Embedded analytics is invisible infrastructure inside someone else’s product, and the better you embed, the more invisible and substitutable you become. Invisible means no end user ever demands you by name. No demand pull means no pricing power.

The endgame is public. Logi Analytics, one of the earliest embedded-first vendors, was absorbed into insightsoftware. Yellowfin went to Idera in 2022 and became one of ten brands in a developer-tools portfolio. Invisible companies don’t get to become category kings. They become line items in somebody else’s portfolio.

Intel had the same problem. It was an invisible component inside somebody else’s beige box until it paid PC makers to put a sticker on the case, and buyers started asking for the hidden part by name. Embedded analytics needs its own Intel Inside move: become valuable enough that the host’s customers demand your analytical agent.

Problem 2: The security pitch kills the learning loop. Cube promises “no cross-tenant leakage.” WisdomAI “never trains models on customer data.” ThoughtSpot advertises “zero LLM data retention.”

Every one of these is a real security requirement that real enterprise buyers demand. Good. Necessary.

Also: word for word, a company explaining why it can’t win the market it’s standing in. They’ve turned the absence of a moat into a security feature.

And the secrecy protects less than they think. The moment a user posts “why doesn’t this CLV analysis work” on Reddit, Claude knows. Everything public already feeds the models. The vendor’s own product is the one place the vendor has promised to learn nothing from.

Believe me, I’m a product person. The alternative is the most expensive learning loop imaginable: let the product fail ten times, then pay someone like me to notice the pattern by hand.

Problem 3: The companies best placed to win are built not to move. Problem 1 makes embedded hard to sell fast, nobody asks for what they can’t see, unless you already have an in with the customer. At least on the enterprise side, incumbents selling both traditional and embedded analytics start with the one advantage pure-plays would kill for: distribution.

And that is precisely why they won’t rebuild around it. Sisense, GoodData, ThoughtSpot, Qlik, Tableau: they all build agents for the internal enterprise analyst first and expose embedding as a secondary SDK. The learning loop stays sealed inside each enterprise, by architecture, because that’s who the org is built to serve. And the internal bet is paying: by their own numbers, ThoughtSpot’s platform usage is up 133% year over year, with Spotter running at 64% of all customers. Success is the sedative. Embedded stays the stepchild upsell, not the prize worth solving the first two problems for.

Of the three, I think the market misunderstands the second most: everyone treats isolated data and isolated learning as the same thing. They’re not.

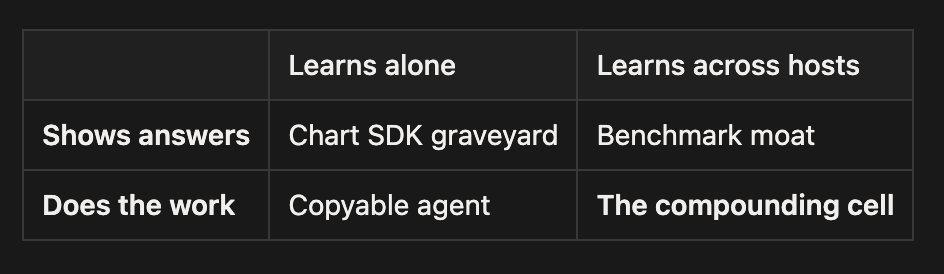

There are only four places to stand. Only one compounds.

Two questions sort every player:

How agentic is it: Does your product show answers, or do the work?

How does it learn: Does it learn alone, one deployment at a time, or learn across hosts?

The chart SDK graveyard. Luzmo, Qrvey, Embeddable, and friends. “Embed our dashboards” collapses into “the host’s own devs ask Claude for the charts.” The obituary is already public: Explo, a chart-SDK pure-play, was absorbed into Omni in October 2025, with customers migrated off the standalone product within twelve months.

The copyable agent. Per-tenant agents look like the future. They talk, they reason, they act. But each one learns inside exactly one deployment, so the part that transfers is generic reasoning. And generic reasoning gets cheaper with every model release. Useful, sellable, copyable.

The benchmark moat. “You versus the 4,000 other companies on this platform.” A foundation model can’t hallucinate that number, and no single host can see it. That’s a genuine moat, the only one on the “shows answers” row. But you’re still selling a surface a human reads before deciding. A moat with a low ceiling.

The compounding cell. The embedded autopilot that does the customer’s analytical work, acts inside the product, and learns which moves actually work across every host it lives in.

Not “show me my churn.” More like:

“Companies like yours usually fix this churn pattern by changing these three workflows. Try this one first.”

The winner doesn’t need the hosts’ data to say that. It needs what worked. The next host gets no rows and no tenant secrets from anyone. It gets a better prior: for this pattern, those three workflows usually win.

Raw data stays home. What crosses hosts is what worked. That turns the security pitch from a cage into a deal: opt in, and your agent arrives already knowing what no single host can learn alone.

Two locks guard this position. The host can’t rebuild it: it only ever sees its own product. And the foundation model can’t eat it: the outcomes of those workflow changes never go public. They live inside private product loops, out of reach of anything trained on the public internet.

Every new host makes the autopilot smarter. Every improvement wins the next host. That’s the compounding.

That cell is empty.

And the market is moving, just not toward it. Explo folded into the graveyard’s consolidation. GoodData’s entire AI pivot, from the Understand Labs acquisition to the MCP server to its own agents shipping through 2026, is a climb from showing answers to doing the work, strictly inside per-deployment walls. The new per-tenant agents: the same climb.

Every move is vertical. Nobody moves right.

If you’re building, build where the learning compounds.

If you’re job-hunting in data, go stand in the empty cell before it has a name.

If you run analytics at an incumbent, stop treating embedded as the SDK attached to the real product. The stepchild is about to be worth more than the family business.

I’m no VC. But if I were, I’d tell you to call me when you find one of those ;)