Default Funded or Default Dead

Why Airbyte raised with 15 months of runway left.

Conventional fundraising wisdom says start raising six months before you run out of money. If you raised 24 months of runway, that means month 18. Plenty of time to hit metrics, prove PMF, then raise from strength.

This is backwards. You’re not raising from strength at month 18. You’re raising from schedule.

Airbyte, the Open-Source ETL Tool, raised their Series A three months after closing seed—with 15 months of runway still in the bank. They didn’t need the money. They had edge: usage was exploding, the right partner showed up, and they could say no to bad terms. So they moved.

The founders who waited until month 18? Many of them hit a market that had turned cold. Same pitch, same metrics, vastly worse outcomes. Down rounds nearly quadrupled between Q1 2022 and Q1 2023. Startup shutdowns jumped 62%. These weren’t worse companies. They were companies that raised on schedule instead of raising on edge.

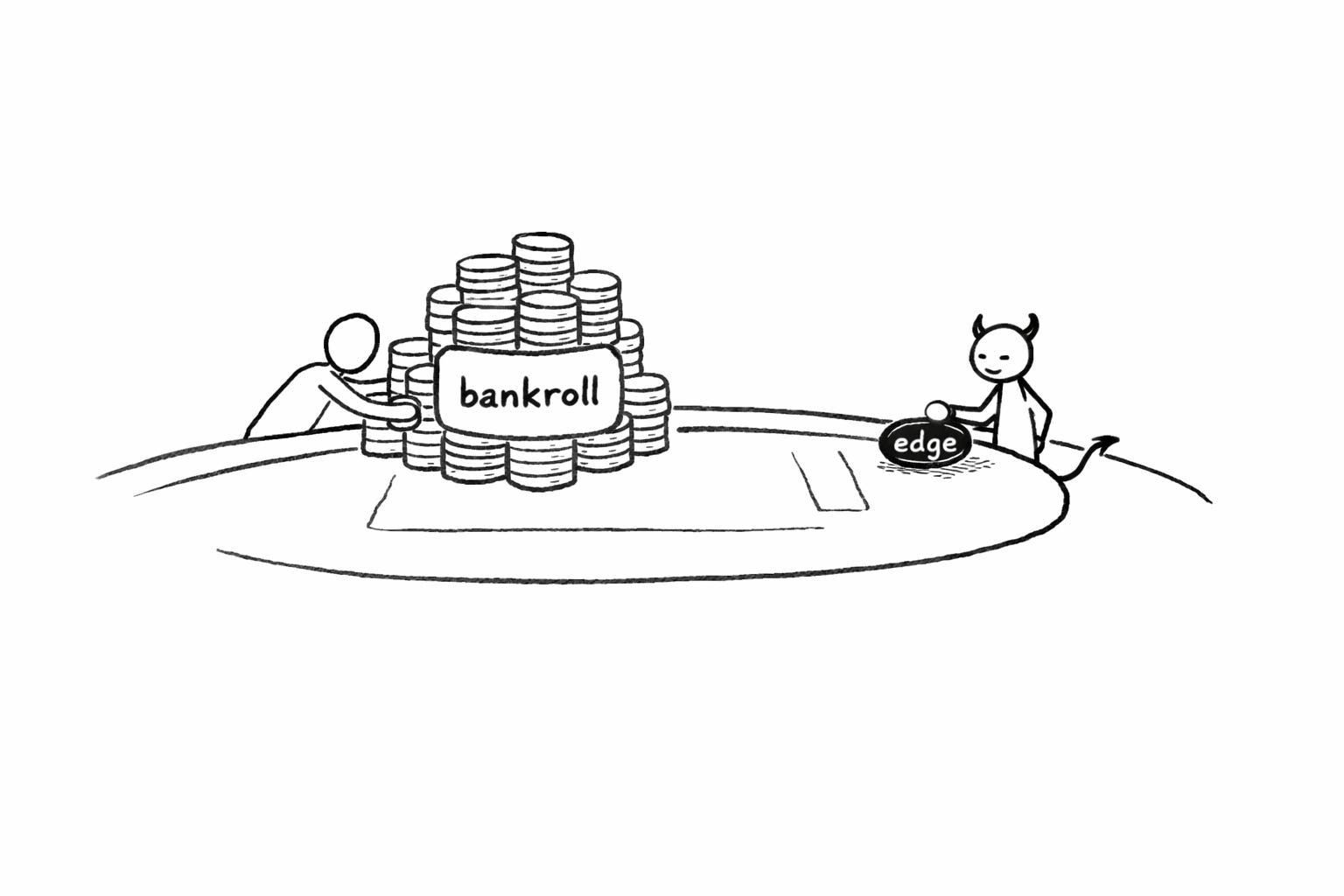

Professional gamblers have a rule for this. It’s called Kelly Criterion: only bet when you have positive expected value, and size your bet to your edge. If you don’t have edge, the optimal bet is zero—regardless of how much bankroll you have.

For founders, runway is your bankroll. It tells you how long you can play. It doesn’t tell you when to play.

Runway isn’t your trigger. Edge is.

Kelly Criterion for Founders: Why “Raise When You Need It” Is Mathematically Backwards

Professional gamblers don’t bet when they have money. They bet when they have edge.

This is Kelly Criterion in one sentence: only bet when you have positive expected value, and size your bet proportionally to your edge. The math is brutal in its implications. If you don’t have edge—if the conditions don’t favor you—the optimal bet is zero. Not a small bet. Zero. Regardless of how much bankroll you have.

For founders, your runway is your bankroll. It tells you how long you can play. It doesn’t tell you when you should play.

The conventional wisdom violates Kelly completely. “Raise when you need it” translates to “bet when your bankroll forces you to.” Kelly’s math predicts exactly what happens next: you enter the market at your weakest moment. Investors sense the desperation. Your leverage evaporates. The terms you get reflect your lack of options, not your company’s potential.

And here’s where it gets worse. Kelly violations compound. A bad raise from a desperation position doesn’t just hurt once. The dilution guts your ownership. The liquidation preferences eat your upside. The wrong investors poison your cap table. The valuation you accept becomes the ceiling for your next round. You’re not just losing one bet. You’re degrading your ability to win every future bet.

The 2022-2023 fundraising massacre proved Kelly’s prediction at scale. Down rounds nearly quadrupled in a single year—from 5.2% of all rounds in Q1 2022 to 18.7% in Q1 2023. Same companies. Same founders. Same business models. Different market timing. The founders who raised in early 2022 had edge—the market was eager, competition for deals was fierce, terms favored founders. The founders who waited until their runway forced them into the market got crushed.

Startup shutdowns told the same story: 467 in 2022, then 761 in 2023—a 62% increase. These weren’t worse companies. They were companies that bet without edge because their bankroll told them to.

That’s not a planning failure. That’s a Kelly violation The market didn’t care about the spreadsheets.

Fractional Kelly: What Airbyte Understood

Airbyte raised their Series A three months after closing their seed round.

They had 15 months of runway still in the bank. The spreadsheet said they had nearly two years before they needed to think about this. By every conventional metric, raising was premature. Unnecessary. Maybe even irresponsible—why take dilution you don’t need?

Here’s why: they understood fractional Kelly.

Professional gamblers don’t even use full Kelly—they use “fractional Kelly,” betting one-half or one-quarter of what the formula suggests. Why? Because edge estimation is uncertain. Markets shift. Conditions change. Fractional Kelly reduces volatility and preserves optionality for future bets. You’re not just optimizing this bet; you’re protecting your ability to make the next bet from a position of strength.

Airbyte’s translation: raise when edge is present, even if you don’t “need” the money. Preserve optionality for the months when edge disappears.

I asked Jean Lafleur, Airbyte’s co-founder, what drove them to move so fast. His answer was a masterclass in recognizing edge:

Signal: “Very strong pull from the market—open-source usage was a huge hockey stick.” Their Docker pulls went from 2,500 to 40,000 in three months. The curve spoke for itself.

Timing:“We found great partners with Benchmark, who went through this already several times—Chetan was at the board of Mulesoft, Elastic and Mongo—and who were already contributing a lot strategically. So we wanted to formalize that partnership.” The right partner showed up. That window doesn’t stay open.

Leverage: “We didn’t need the money per se.” They could be selective. They could say no. That’s not a nice-to-have—that’s the difference between founder-friendly terms and getting squeezed.

Here’s the part that matters most: they didn’t plan the timeline. When I suggested they’d set a deliberate 9-month deadline to force fast decisions, Jean corrected me: “Market was on fire, perfect partner showed up, we grabbed the opportunity—didn’t plan the 9-month timeline, it just made sense when it happened.”

That’s Kelly in action. They weren’t following a playbook. They weren’t raising because their runway told them to. They recognized when all three conditions converged—and they moved.

Same stage, same market, opposite outcome from the founders who waited. Airbyte became a unicorn. The founders who followed the Month-22 playbook became a statistic.

Signal, Leverage, Timing: The Three Conditions That Mean Your Window Is Open

Edge isn’t a feeling. It’s three conditions you can measure.

Condition 1: Signal. Do you have proof that something is working?

Signal means metrics that tell a story without you having to sell it. MRR growing 15-20%+ month-over-month for three or more consecutive months. Retention curves that flatten instead of decay. Organic acquisition accelerating—word-of-mouth, referrals, inbound interest you didn’t pay for. Investors reaching out to you without a pitch.

The test is simple: if you showed your last 90 days of data to an investor with zero context, would they lean in—or would they ask what else you have?

Airbyte’s signal was unmistakable. 16x growth in Docker pulls over three months. No explanation needed. The curve spoke for itself.

Condition 2: Leverage. Can you negotiate from strength, not desperation?

Leverage comes from options. Multiple investors expressing serious interest—not “let’s keep talking,” but term sheets or clear intent. Twelve or more months of runway remaining, so you can walk away from bad terms without dying. Alternatives if your top-choice investor passes.

The test: if your preferred investor said no tomorrow, would you have comparable alternatives at similar terms? Or would you have to take whatever you could get?

Airbyte had leverage because they didn’t need the money. They could be selective. They could say no. That’s not a nice-to-have. That’s the difference between founder-friendly terms and getting squeezed.

Condition 3: Timing. Is the external environment favorable?

Timing is everything you don’t control. VC deployment cycles—January through May and September through November are peak windows; summer and December are dead zones. Sector sentiment—is your category “hot” or facing headwinds? Public market health—when public markets tank, private markets follow with a lag. Recent comparable raises—has a competitor or adjacent company raised successfully in the last 90 days, validating the space?

The test: if you started raising today, would the market environment help you or hurt you?

Timing killed more companies in 2022-2023 than bad products did. The founders who raised in Q1 2022 rode a favorable wave. The founders who waited nine months entered a completely different market—same pitch, same metrics, vastly worse outcomes.

Your window is open when all three conditions are present. Signal, leverage, and timing. When they converge, raise—even if you have runway to spare. Even if your spreadsheet says it’s not time yet. This is your Kelly moment. You have edge. Use it.

Your window is closed when any one is missing. Don’t raise. Don’t “test the market.” Don’t start conversations you can’t finish. You’d be betting without edge, and Kelly’s math is unforgiving. Wait. Build signal. Extend runway if you have to. Protect your ability to raise from strength when the window opens again.